The Role of Flexibility in Europe's Energy Transition

Europe’s electricity system is at a pivotal moment. As the continent accelerates toward a more sustainable future, energy supply is undergoing a deep transformation, with renewable energy sources replacing conventional generation. On the demand side, electrification is becoming the backbone of decarbonisation across sectors, from residential, to mobility and industry. This shift is not only increasing the overall electricity demand, but it is also reshaping when, where, and how electricity is consumed. These parallel evolutions are creating new challenges for infrastructure, energy system stability, and market design.

Europe’s electricity system is at a pivotal moment. As the continent accelerates toward a more sustainable future, energy supply is undergoing a deep transformation, with renewable energy sources replacing conventional generation. On the demand side, electrification is becoming the backbone of decarbonisation across sectors, from residential, to mobility and industry. This shift is not only increasing the overall electricity demand, but it is also reshaping when, where, and how electricity is consumed. These parallel evolutions are creating new challenges for infrastructure, energy system stability, and market design.

The interplay between demand growth, infrastructure limitations, and the nature of renewable generation is driving flexibility and demand-side response (DSR) from being optional features to becoming essential pillars of a resilient energy system.

Renewables and energy supply variability

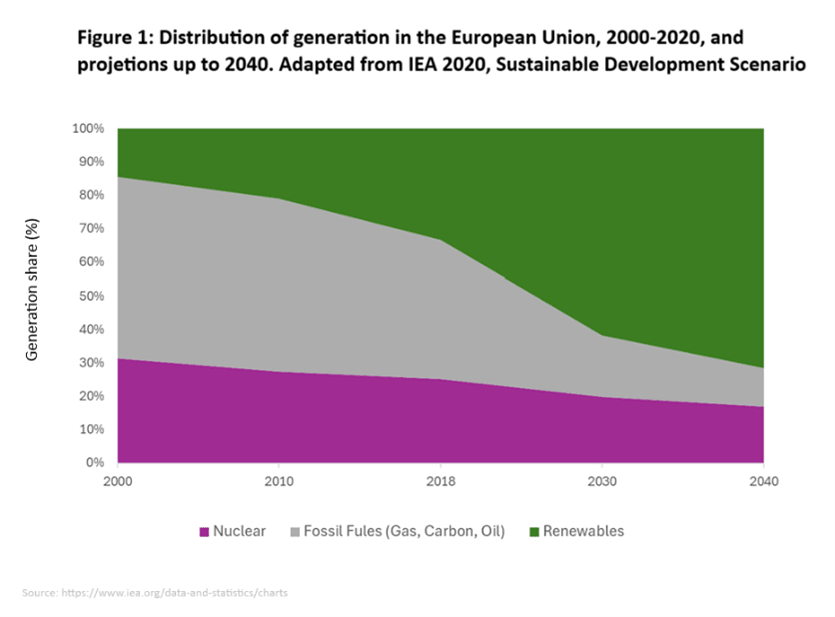

The shift to renewable energy is central to Europe’s decarbonisation ambition. Wind and solar are now dominating new installed capacity, and their share in the generation mix continues to grow. Unlike conventional power plants, renewable energy sources are inherently variable. Their output depends on weather conditions, daily and seasonal cycles, which introduces a new degree of inconsistency into the system.

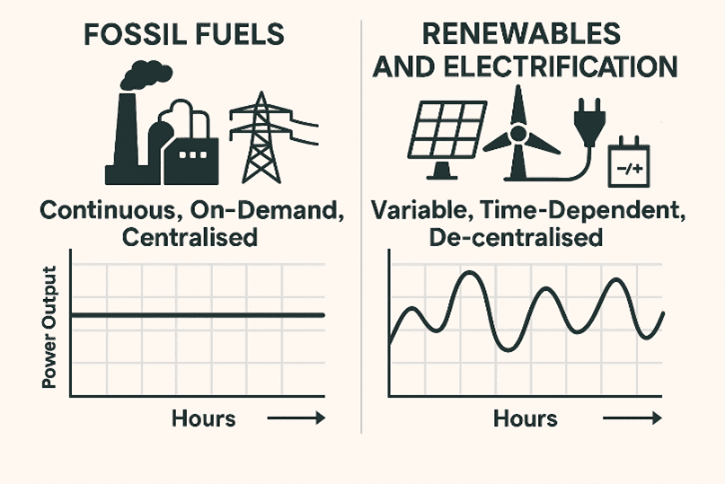

Solar generation peaks during daylight hours and is strongest in summer, while wind output can fluctuate dramatically from hour to hour. These patterns do not always align with consumption, which tends to peak in the early evening and during colder months. As a result, the system experiences more pronounced base-peak differentials, with periods of surplus followed by periods of scarcity.

Solar generation peaks during daylight hours and is strongest in summer, while wind output can fluctuate dramatically from hour to hour. These patterns do not always align with consumption, which tends to peak in the early evening and during colder months. As a result, the system experiences more pronounced base-peak differentials, with periods of surplus followed by periods of scarcity.

While wholesale energy prices are driven by scarcity or abundance, variability in energy availability impacts more than just pricing. The physical system must still maintain its balance in real time. When renewable output drops unexpectedly or demand surges, the grid must have sufficient flexibility to respond. Without it, the risk of curtailment, load shedding, or even outages increase.

Grid infrastructure readiness in the new electrification era

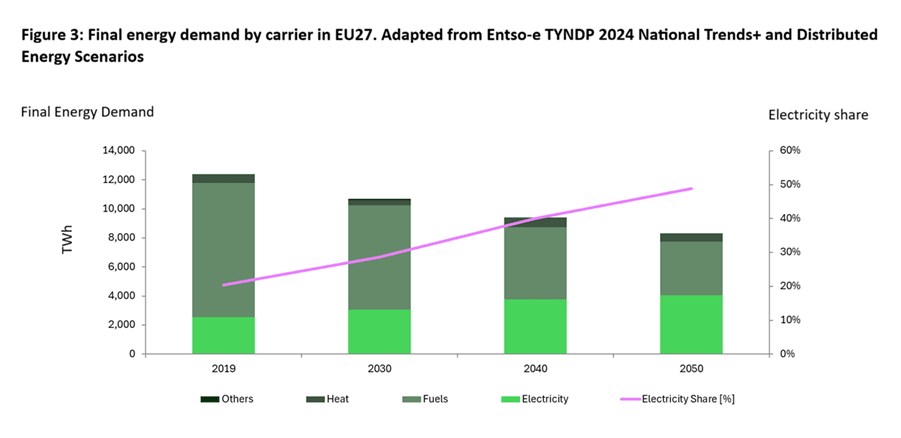

Electricity demand in Europe is rising steadily, driven by the public and private sector’s decarbonisation targets and the consequent push to electrify sectors that have been traditionally powered by fossil fuels, i.e. mobility, residential and commercial heating, and industrial process heat. However, this growth is not uniform. It introduces new demand peaks, shifts in daily and seasonal consumption patterns, and regional disparities that traditional infrastructure was not designed to handle.

The existing grid system in Europe was built around predictable, centralised generation and relatively stable demand. Today, it must accommodate decentralised energy sources, bidirectional flows, and increasingly dynamic consumption. Distribution networks are under pressure as more devices and systems connect at the edge of the grid. Transmission corridors are also strained, especially as renewable generation is often located far from demand centres.

Upgrading physical infrastructure is a long-term and capital-intensive process, and networks are already behind fast-tracking new connections. System operators are turning to digital solutions, real-time monitoring, and market-based mechanisms to manage congestion and maintain reliability.

As energy systems grow more complex and require ever-faster reactions, digitalisation becomes not just an enabler but the only viable path forward. While system operators deploy advanced digital tools to manage congestion, private organisations face a parallel challenge: adopting flexibility solutions grounded in automation and data intelligence. Both sides depend on real-time information, advanced analytics, and the ability to participate dynamically in markets—making investment in digital technologies and digital skills essential across the entire energy ecosystem.

Resilience beyond economics: the rise of demand side response and flexibility markets

Historically, electricity markets have relied on price signals to guide investment and operational decisions. But in a system dominated by variable renewables, price alone cannot guarantee physical resilience, as wholesale spot prices do not procure frequency response, voltage control, inertia, particularly under low marginal cost conditions the ability to absorb fluctuations, respond to imbalances, and recover from disturbances not only helps limit capital requirements, but becomes a technical imperative.

Resilience now encompasses more than just backup generation. It includes storage technologies, grid automation, and the ability to modulate demand. Flexibility, whether through shifting consumption, storing excess energy, or coordinating distributed assets, is emerging as a key enabler of system stability.

This shift reframes the conversation: from one of economic optimisation to one of operational necessity – optimised through economics. Flexibility is no longer a marginal feature, it is central to the functioning of a low-carbon electricity system.

In this context, demand-side response (DSR) and flexibility markets are gaining prominence across Europe. DSR – through independent aggregation and optimization, distributed generation - allows consumers and flexumers from various end-use sectors (residential, commercial, and industrial) to adjust their electricity usage in response to grid conditions or price signals. This can mean reducing consumption during peak hours, shifting usage to times of surplus, or even providing ancillary services.

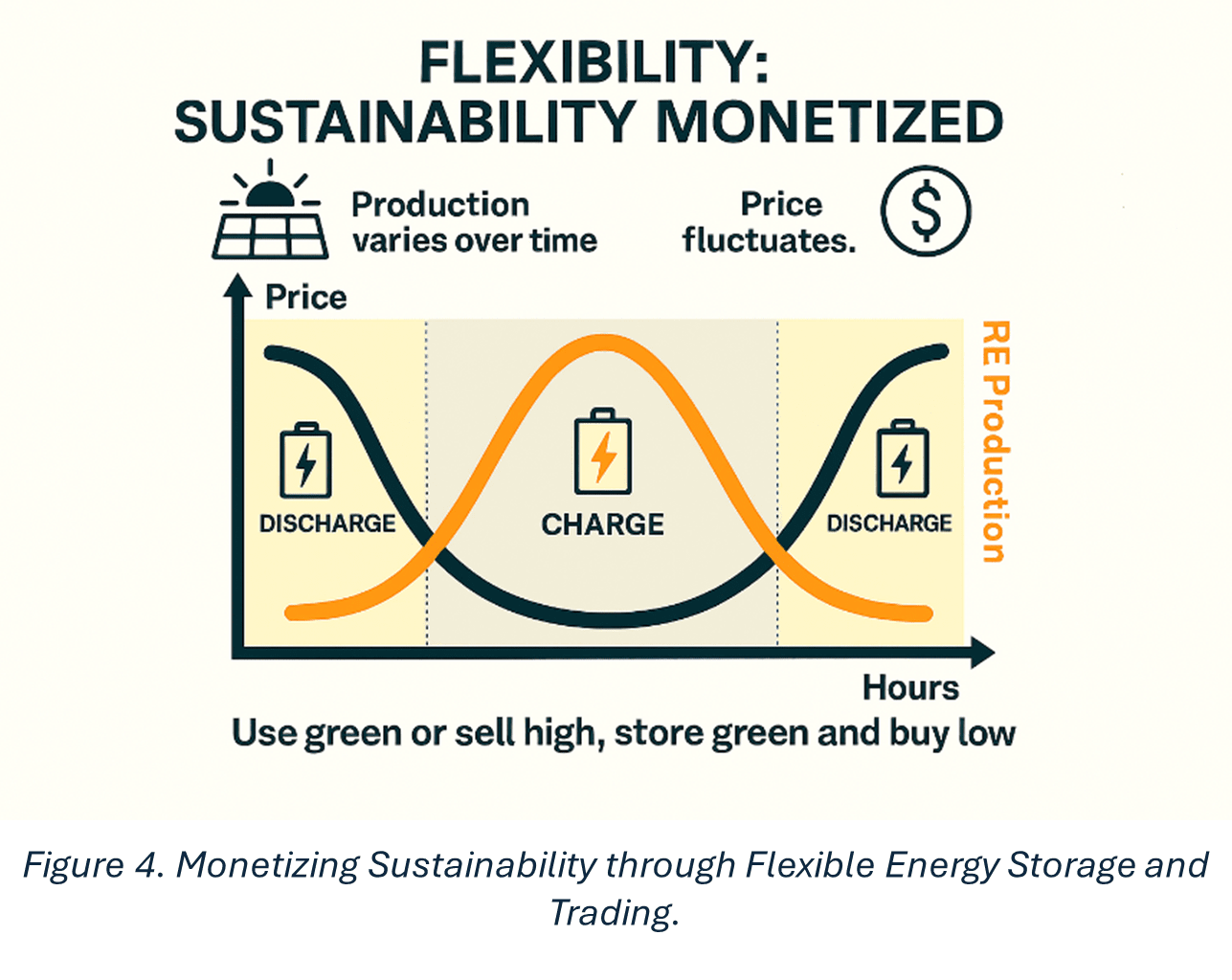

Flexibility markets are emerging to monetise these capabilities. Local platforms allow distributed energy resources to participate in balancing and congestion management. Aggregators bundle small-scale assets into marketable portfolios. Regulatory frameworks are evolving to support active consumers and new business models.

While progress varies by country, the direction is clear. Flexibility is being integrated into market design, grid operations, and policy frameworks. A key example of this is the gradual shift toward shorter market settlement intervals, such as 15-minute settlement periods, across several European power markets. By aligning market settlement more closely with real system conditions, shorter intervals improve the visibility and valuation of flexibility, particularly on the demand side. They allow imbalances, ramps, and short-term variability to be reflected more accurately in price signals, creating clearer incentives for consumers and aggregators to adjust consumption in line with system needs. In this way, settlement reform does not introduce flexibility as a new concept, but enables existing flexible capabilities to be activated, measured, and rewarded more effectively. Whether these tools will prove sufficient to counter the scale and speed of change in the European grid is yet to be seen. It is, nonetheless, essential that organisations and their processes do not become the bottleneck in this transition.

While progress varies by country, the direction is clear. Flexibility is being integrated into market design, grid operations, and policy frameworks. A key example of this is the gradual shift toward shorter market settlement intervals, such as 15-minute settlement periods, across several European power markets. By aligning market settlement more closely with real system conditions, shorter intervals improve the visibility and valuation of flexibility, particularly on the demand side. They allow imbalances, ramps, and short-term variability to be reflected more accurately in price signals, creating clearer incentives for consumers and aggregators to adjust consumption in line with system needs. In this way, settlement reform does not introduce flexibility as a new concept, but enables existing flexible capabilities to be activated, measured, and rewarded more effectively. Whether these tools will prove sufficient to counter the scale and speed of change in the European grid is yet to be seen. It is, nonetheless, essential that organisations and their processes do not become the bottleneck in this transition.

Since the industrial revolution, our economies have relied on fossil fuels and on consumption behaviours shaped by abundant and on-demand energy, essentially the opposite of flexible. With the increasing capacity and cost competitiveness of renewable energy, combined with the rapid electrification of end-uses, we have entered a new transitional phase. Modern industrial sites or vehicles often rely on multiple energy carriers (such as combustible fuels and electricity), technologies (e.g., gas and electric boilers or hybrid cars), and supply systems (on-site generation and the grid).

In these hybrid ecosystems, behavioural changes in how users consume energy are essential. Handling the variability of renewable generation, the coexistence of diverse energy carriers, and a more dynamic energy system requires more elastic demand profiles and adaptive consumption patterns from the end-users.

Flexibility supports this behavioural shift and plays a critical role in enabling the energy transition, beyond grid stability or the monetization opportunities offered by energy markets. For example, by adopting flexibility, consumers can better integrate clean technologies and support the gradual reduction of the grid’s reliance on fossil fuels. Energy consumption can be shifted based on the carbon intensity of electricity, scheduling energy intensive operations when low carbon electricity is abundant and competitively priced. Additionally, flexibility facilitates the integration of key technologies that enhance the stability, resilience, and security of energy supply, including batteries, thermal energy storage, onsite generation, electric vehicles, combined heat and power (CHP) systems, and microgrids.

Conclusion

Europe’s electricity system is being reshaped by two converging forces: the rapid rise of renewables and accelerating electrification across end-use sectors. The variability of renewable generation and growing peak loads are exposing the limits of legacy infrastructure and traditional market design.

As consumption and generation become increasingly decentralized—through on-site renewables, EV charging, storage, and microgrids—Distributed Energy Resources (DERs) are expanding the flexibility available to the system. Unlocking this potential requires advanced, digital energy management solutions that enable real-time monitoring, forecasting, and automated control.

Across Europe, new market models are emerging to integrate flexibility into grid operations. Demand-side response and flexibility markets allow consumers to actively support system balance, reduce the need for costly grid reinforcements, and accelerate renewable integration.

Flexibility is becoming a cornerstone of Europe’s energy transition. It not only strengthens system stability, but also enables a more resilient, efficient, sustainable and increasingly a financially attractive way of consuming and producing energy.

To learn more about how SE Advisory Services can help your business, get in touch with our experts Balint Fabok and Silvia Madeddu now.

Contributors:

Balint Fabok - Associate Director - Solution Architect

Silvia Madeddu - Solution Architect Team Leader

David Laszlo - Lead Consultant, Global Solutions Consulting

Mikel Bilbao - Associate Solution Architect