Rethinking Risk: Is Now the Time to Invest in Renewable Energy?

- Meister Eckhart-

The German mystic’s sentiment seems to have stood the test of time for 700 years, yet, quantifying costs is always critical to decision making, and today it is fraught with complexity.

Ongoing geopolitical instability, regulatory uncertainty, and trade disputes are reshaping today’s global supply chains—impacting nearly three-quarters of international trade1. At the same time, extreme weather events are adding to the burden, making strategic planning increasingly complex and opaque for business leaders. In 2024 alone, such weather events caused an estimated $368 billion in economic losses, primarily in the U.S. and Europe2.

Ongoing geopolitical instability, regulatory uncertainty, and trade disputes are reshaping today’s global supply chains—impacting nearly three-quarters of international trade1. At the same time, extreme weather events are adding to the burden, making strategic planning increasingly complex and opaque for business leaders. In 2024 alone, such weather events caused an estimated $368 billion in economic losses, primarily in the U.S. and Europe2.

The persistence of these factors ratchets up the pressure on companies to anticipate, respond to, and rebound from acute external events, while delivering value to shareholders and meeting their business objectives, including their sustainability targets and resilience strategies.

As technology has matured, and the cost of wind, solar, and storage has dropped over the last decade, procuring renewable energy has become a surefire way to tick several of these boxes and to help decarbonize emissions.

To make informed decisions on when, where, and how to buy renewables in the current climate, we examine the fundamentals that influence the trajectory of project availability and prices.

Supply - Potential implications of a shift towards a fossil-fuel agenda

More expensive raw materials and components, (i.e., steel for wind turbines,) driven by the slew of tariffs proposed in the U.S., may lead to rising inflation and, in turn, likely higher interest rates. Renewable energy is capex heavy and therefore, on a percentage level, the cost is disproportionately affected by higher interest rates.

“New-build renewable energy projects may struggle to get funding in an environment with increasing borrowing costs, because this will affect the price that the seller needs for their power,” said John Powers, Vice President, Renewable Energy & Cleantech at Schneider Electric, via a recent webinar on the state of renewables.

Additionally, proposed legislative action to re-examine tax credits under the Inflation Reduction Act (IRA), worth hundreds of billions of dollars, would further challenge the buildout of clean technologies including wind and battery storage in the U.S.

The IRA has spurred nearly half a trillion dollars in clean energy investments over the past few years. Both established companies and new market entrants have been able to take advantage of this momentum through generous tax credits. As an advisor, Schneider Electric represents over $10 billion in tax credit investments in the U.S. and has facilitated $1.7 billion in tax credit transfer transactions across 18 deals since late 20233.

From a macroeconomic standpoint, slower U.S. GDP growth, as predicted by economists, may drive up electricity prices. During our recent webinar on U.S. energy policy4, Senior Policy Associate at BNEF, Derrick Flakoll, explained that since a sizeable portion of U.S. natural gas is a by-product of crude oil extraction, lower crude oil demand could create upward pressure on natural gas prices, thereby impacting U.S. power prices since they track gas prices.

Demand - Skyrocketing data center demand will snatch up supply, likely driving renewables’ prices higher

Energy demand from AI data centers will quadruple by 2030, according to the IEA.5 IEA executive director, Fatih Birol, has indicated that “with the rise of AI, the energy sector is at the forefront of one of the most important technological revolutions of our time”.

The infrastructure decisions being made today for AI development will critically shape global electricity demand trajectories beyond 2030. According to recent analyses, the rapid expansion of AI workloads—projected to triple data center electricity consumption to as much as 1,500 TWh by 2030—poses a significant risk of regional power shortages with global repercussions.

The International Monetary Fund and RAND Corporation both warn that without synchronized investments in clean energy and grid modernization, the accelerating demand could outpace infrastructure readiness, leading to localized energy bottlenecks. While efficiency breakthroughs, such as those pioneered by DeepSeek, offer promising mitigation pathways, experts agree that efficiency alone cannot offset the scale of AI’s energy appetite. As Schneider Electric’s Sustainability Research Institute6 emphasizes, the challenge lies not only in managing demand but also in ensuring that energy supply systems evolve fast enough to support the AI revolution sustainably.

Data centers are dominating power demand in the U.S. (anticipated to make up the largest share of the projected increase in global demand) in the near term, requiring dispatchable resources of power, while the interconnection cues are primarily full of wind, solar and battery storage, Flakoll outlined.

Across the Atlantic, the EU is also grappling with attracting investment to maintain its strategic autonomy in critical industrial sectors and science, while mitigating the growing environmental impact of data centers. The EU’s AI Continent Action Plan7 is focused on building large-scale AI data and computing infrastructure, including-setting up AI Gigafactories, which have four times more chips than current AI factories.

Regulations like the Energy Efficiency Directive (EED) are requiring mandatory reporting and the use of renewable energy for data center. However, the sector has already been self-regulating under the Climate Neutral Data Center Pact (CNDP),8 which has led to a diffusion of sustainability practices. For example, Schneider Electric has advised leading co-location providers, including Equinix and Digital Realty, on over 2 TWh of renewable electricity through Corporate Power Purchase Agreements (PPAs) in Europe.

Given a data center's ability to plan their stable energy consumption over a prolonged period, and to provide financing, Régis Castagné, Managing Director at Equinix France said that creating new sources of energy is a duty data centers must fulfill, via a previous video interview on industry trends.9

And of course, many customers have their own sustainability targets. Major tech companies tend to be the largest clean energy buyers, according to Bloomberg10, which require their data center providers to help fulfill their targets or lose out to competitors.

Renewable energy markets – play or nay?

In an environment with significantly rising electricity demand, possible supply crunches, as well as more stringent compliance frameworks, companies that hold off engaging in the market may risk losing out on potential opportunities.

The proposed revision of GHG’s Scope 2 Guidance to introduce mandatory time and location accounting would have serious implications on how companies can credibly buy renewables to count towards their overall decarbonization targets. The GHG Protocol underpins most voluntary reporting frameworks, including the Science Based Targets Initiative (SBTi) and RE100.

Considering these changes, “grandfathering” is a respite that companies can capitalize on. SBTi confirmed that they will allow grandfathering contracts signed before the new Corporate Net-Zero Standard, Version 2.0 comes into effect from 2027, meaning signatories’ projects will be protected11.

Within the next five years, many companies are expected to decarbonize their direct and indirect controlled emissions, or Scope 1 and 2. Just under half of all 400+ RE100 members (45%) have targets between 2025-203012.

One of the easiest ways for companies with 2025 targets to cover their remaining load is with Energy Attribute Certificates (EACs), like Guarantees of Origin (GOs) in Europe or Green Electricity Certificates-(GECs) in China. Presently, GOs are the cheapest they have been since 2021, and products such as long-term GO strips are more readily available in the market, too. Having supported more than1,800 clients with EACs, we have seen that unbundled certificates can be simpler to manage from a compliance perspective. In some cases, they can also be cheaper than those bundled with supply contracts.

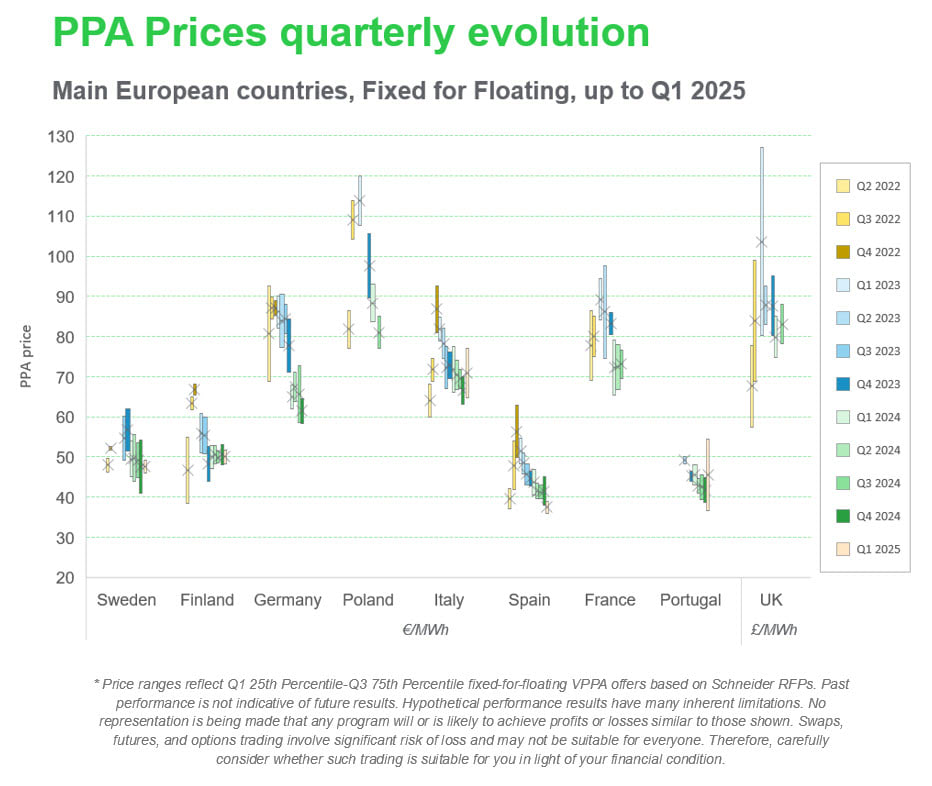

A 2030 target window, however, enables more risk-managed, long-term forward buying options. Companies can strategically layer in other solutions into their portfolio like Corporate PPAs. Corporate PPA prices have come down in major European countries, with sub-EUR 40 PPAs in Spain, the lowest they have been in several years (see graph above). A full process from start to finish of a newbuild renewable energy project can take 18-30 months, so starting early provides the best chance of hitting targets.

For those companies that have a smaller Scope 2 footprint, or who would prefer to transact with lower risk, they may explore options to join an aggregated PPA (with a cohort of suppliers, for example) and commit a smaller portion of their electricity volume to the PPA, while still gaining exposure and knowledge. Long-term EAC strips or short-term PPAs may also cover remaining electricity volumes.

In the U.S., accelerating tax credit transactions (with proper risk mitigation) while they’re still available, is the most pressing move. Many larger developers have stocked up on components in preparation of executive actions, so taking remaining inventory now will be most cost-effective.

Quickly assessing specific market opportunities: e.g., securing transmission discounts through self-production offsite projects in Brazil before proposed market reforms kick-in, or entering markets that have opened new schemes like Direct PPAs in Malaysia and Vietnam can provide additional benefits and a first mover advantage.

In a rapidly evolving energy landscape, companies that act decisively—whether by locking in long-term PPAs, leveraging tax incentives, or seizing emerging market opportunities—will be positioned to manage risk, reduce emissions, and secure cost-effective electricity for the future. The window to act is open, and we encourage businesses to consider the different market opportunities on the horizon.

Click here to connect with a Schneider Electric Sustainability Business renewable energy expert.

.

Contributor:

Aleksandra Klassen, Manager, Renewable Energy & Carbon Advisory, Schneider Electric

.

Sources:

1. Global value and supply chains | OECD

2. Climate and Catastrophe Insight - Aon Report

4. The First 100 Days: What Happened & What's Next for US Energy Policy

5. Energy and AI – Analysis - IEA

6. Artificial Intelligence and electricity: A system dynamics approach | Schneider Electric

7. European Commission AI Continent Action Plan Press Release

8. Climate Neutral Data Centre Pact

9. Interview with Régis Castagné, MD at Equinix France | Schneider Electric

10. 1H 2025 Corporate Energy Market Outlook: Enter Nuclear | BloombergNEF

11. The Impact of the SBTi's New Corporate Net Zero Standard - Sustainability Magazine

12. RE100 Annual Disclosure Report, 2024